- Eliminate the noise: Just Build Wealth

There are a dizzying number of suggestions online on how you should manage your clients’ investments and financial plans. Plenty have been consolidated and rated. The paradox of choice comes to mind right now. As Mr. Schwarz so eloquently puts it in his TEDx talk, when we have too many choices, we can’t make a choice; When considering the tools for financial planning, you are overwhelmed with the choices you must make.

One way a financial advisor can operate their financial planning is to utilize one of the many available software packages. There is a reddit thread that comments on multiple software packages available to financial advisors. The paradox of choice again.

After years of agonizing about exactly how to help clients achieve their goals, I have come up with a simple solution, fitting of Occam’s Razor.

There are four simple steps to just build wealth: (1) Earn more than you spend; (2) Establish a Cash Reserve; (3) Invest the rest long term; and (4) pay attention to taxes. That’s it! By following these four simple steps, you will build wealth.

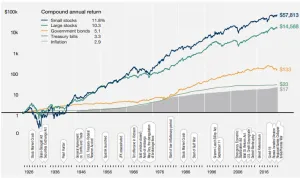

2. Understanding historical rates of return.

In this interview, Roger Ibbotson tells of how his and Rex Sinquefield’s groundbreaking research on returns of the public financial markets began to inform the public of just what historical rates of returns have been. This is instructive for the investor, because, using this data set and a longer-term time horizon, you can begin to get an understanding of long-term rates of return. You can use this to project future asset values with confidence.

3. Apply risk management: Use familiarity bias to manage human emotions during downturns in the markets.

Resist the temptations of mutual funds and exchange-traded funds. Own individual stocks with household names. This is not about great performance; it’s about keeping clients in the game when markets are angry.

Remember this: Stock Market Crash of 2008

When this happens, your client might want to sell their stock market holdings! But will they lose confidence in those companies from whom you buy things? Because of familiarity bias, whether it’s Microsoft, Proctor & Gamble, Apple, or Costco Wholesale, these companies give you a good feeling that often transcends the crisis mentality about “the market”. Holding on to these investments encourages clients to just build wealth.

Your client might not like “The Market”, but that doesn’t mean she wants to sell one of her well-known company’s stocks. Instead, she will sell a mutual fund. Mutual funds have confusing names and most really don’t tell you what they own. Confusion about exactly what your mutual fund owns, especially when markets are in decline, plays into that panic and sell impulse. It’s very easy to sell funds because of this.

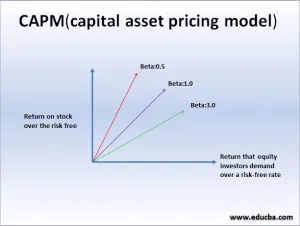

4. Now, use the Sharpe Ratio to manage your bond-stock blend

William Sharpe, an American economist at Stanford, made significant contributions to the field of finance. He was awarded the Nobel Prize in Economic Sciences for developing the Capital Asset Pricing Model (CAPM), a pivotal tool in understanding investment risks and returns.

Another of Sharpe’s contributions to the development of the investment process was the Sharpe Ratio to help investors compare different portfolios both in risk and reward. But the byproduct of such work is a tool to help give insight into stock-to-bond allocations.

If you can focus on the five- or ten-year record, a blend of stocks and bonds can become consistent and predictable way to just build wealth. This is also a better way to determine asset allocation.

A simple rule of thumb for asset allocation established over the years is that your personal percentage in stocks should be 100 minus your age. If you are 30, it ought to be 70%; if you are 70, it ought to be 30%. This might be too simplistic. Instead, decide by what level of a downswing you can handle. 30 years olds in most cases should have 100% in stock unless they are extremely risk averse.

But a better way to use Dr. Sharpe’s equation is to take a multi-year historical view of how the different asset classes blend and try to visualize how you would react to those returns. Over 35 years in this career has told me that nothing substitutes for that moment that you look at your account values and they’re 10-20% lower than they were a day, week, month or year ago. This experience often changes people’s view of market risk.

This is a table put together a few years ago by Morgan Stanley Wealth Management research showing risk and reward for different asset allocations.

So, using these tools, keep it simple. Use individual stocks and bonds and manage allocations with the help of the Sharpe Ratio, you can help your clients just build wealth.

As I said, my investment philosophy to just build wealth is elegantly simple:

1. Earn More Than You Spend.

2. Establish a Cash Reserve

3. Invest the rest long term

4. Pay attention to taxes.

Use the steps above to invest the rest in the long term with public markets. More to follow on taxes and private markets.