- The first step for portfolio management is asset allocation. Creating a portfolio blend that increases portfolio consistency is so important. This blending is called asset allocation.

In 1966 Dr William Sharpe at Stanford, took investor’s portfolio, subtracted from those portfolio’s return percentage the “risk-free rate,” generally the return of the ten-year treasury bond, and then, divided that “excess return” by the variance of that portfolio—how much it differs from its average rate of return. This return-per-unit-of-risk as a metric is an ideal way to compare fund performance. Showcased by its inventor, Bill Sharpe, this metric for judging portfolio performance is now known as a “Sharpe Ratio” and seems to be the best way to compare two portfolio’s performances.

Twenty years later, in 1986 by Gary Brinson, Randolph Hood and Gilbert Beebower studied quarterly returns of 91 large US Pension funds between 1974 and 1983. The study compared these returns to a hypothetical fund that held the same average asset allocation but in indexed investments. BHB had concluded that asset allocation explained 93.6% of variation in a portfolio’s quarterly returns. Said another way, the portfolio performance doesn’t differ based on the choice of one stock or bond versus another as much as what the ratio of stocks to bonds (to cash) is during the studied period.

So, we know asset allocation is the most important step, and Sharpe showed us how returns vary by allocation. If you simply use the stock and bond indices and then over different time periods look at the range of asset allocations, you can use this information in client meetings to discuss how each of these stock/bond mixes perform.

Once you have the asset allocation question settled, move on to stock selection. In our portfolios we use individual US stocks, bonds and cash.

Over 35 years of experience in seven bear markets tells me that investing in known company names will help people make better decisions in lousy markets. This is called using familiarity bias to help with decision making. We all want to own things we know about.

In every single bear market, I have been in (I count seven real bear markets since 1987), clients want to “raise cash” just to make sure they will be okay. When deciding what to get rid of, clients usually sell investments with no name recognition. If your holdings include 10 of the most recognized US companies and the S&P 500 index ETF, the ETF is going to be sold first. It is simply less familiar than those individual names. If you have US holdings and then various and sundry foreign stocks, mutual funds or ETFs, those foreign stocks are going. We human beings like things that are familiar to us, especially in times of stress.

2. Sector weightings: don’t overthink it.

Standard and Poor’s convenes a committee on a regular basis to decide exactly what companies can be in the flagship index. Once they make that decision, companies can be classified into industries. The S&P 500 is currently divided into 11 sectors:

- Communication services

- Consumer Discretionary

- Consumer Staples

- Energy

- Financials

- Healthcare

- Industrials

- Materials

- Real Estate

- Technology

- Utilities

Our portfolios do not attempt to overweight or underweight any sectors, but as time goes on, those who grow faster do become overweight. Over time, we find ourselves using many techniques to work against overweight.

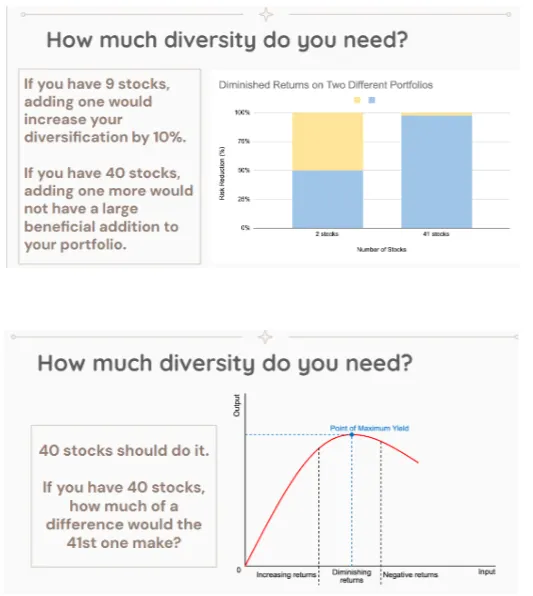

3. We try not to overdiversify.

4. We see no need for non-US companies.

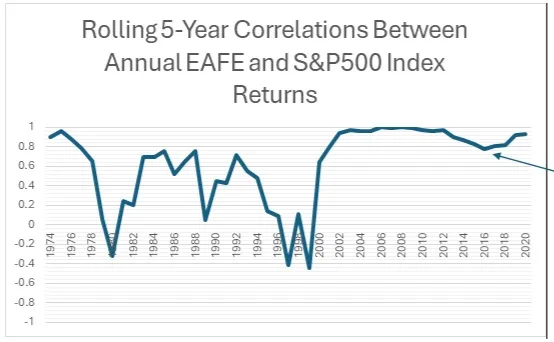

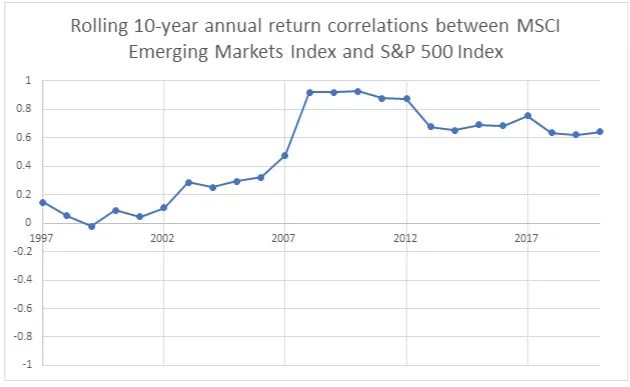

U. S. Investors are counselled to diversify their investments internationally because there has been a belief that these non-US investments improve performance. In other words, non-US investment returns are equally good—perhaps better—that US returns, and their better performance occurs during different times that US markets. This hasn’t happened since the 1990s.

Also, the correlations between US and non-US performance have tightened since the mid 1990s.